How Do You Buy a Home in Atlanta If You're Self-Employed or 1099?

If you're self-employed or paid on 1099 and you've been told buying a home in Atlanta is harder for you, that's not exactly wrong. But it's not the full story either. You can absolutely buy a home as a freelancer, contractor, business owner, real estate agent, gig worker, or 1099 consultant. What changes is how you document your income, which loan products fit your situation, and how far in advance you need to plan.

I work with buyers across Metro Atlanta, and a significant share of them are self-employed. Tech consultants, hair stylists, real estate agents, photographers, doctors with their own practices, content creators, Uber drivers, freelance designers, small business owners. The same questions come up over and over: How much income do I actually need to show? Will my tax write-offs hurt me? Do I have to wait two years? What's a bank statement loan and is it worth the higher rate?

Nearly a decade helping Atlanta buyers means I've watched these answers shift as the lending landscape expanded. The non-QM market has matured. Bank statement loans and 1099-only loans are widely available in Georgia now, and they're priced more competitively than they used to be. Conventional self-employed financing is still the cheapest option if your tax returns support it. The right loan depends on what your income looks like on paper versus what it looks like in your bank account.

Here's what you need to know.

What Counts as "Self-Employed" to a Mortgage Lender

Lenders use a specific definition that's broader than most people assume. For mortgage loans, you're considered self-employed if you own 25% or more of a business, receive 1099 income for services rendered, or your income is documented in the Schedule C part of your personal tax returns.

That covers a lot of people:

Sole proprietors and freelancers who file Schedule C

Independent contractors who receive 1099-NEC forms (real estate agents, hair stylists, consultants, photographers, contractors)

LLC owners and partners

S-corp and C-corp owners with 25% or more ownership

Gig workers (Uber, Lyft, DoorDash, Instacart, Amazon Flex)

Commission-based sales professionals

Small business owners with employees

If any of that describes how you earn income, the standard W-2 mortgage process doesn't apply to you in the same way. Your file will be underwritten differently, and you'll have more loan products to choose from than a traditional W-2 buyer.

The Two-Year Rule (and the Exceptions)

The most common piece of advice you'll hear is that you need two years of self-employment history before you can buy. That's the conventional Fannie Mae and Freddie Mac guideline, and it's mostly true. But it comes with real exceptions that buyers often don't know about.

The standard rule. For a conventional loan, lenders typically want to see two years of self-employment income, documented through tax returns. They average that two-year income to calculate your qualifying figure.

The one-year exception. If you've been self-employed for at least one year and you can show two years of prior employment in the same line of work, you can often qualify with just one year of self-employment tax returns. This is huge for people who went from being a W-2 hair stylist at a salon to renting their own chair, or from a W-2 software engineer to a 1099 consultant in the same field. Same work, different tax treatment, and lenders will recognize that continuity.

Non-QM exceptions. Bank statement loans and 1099-only loans don't always require two years either. Some lenders offer 12-month self-employment programs for borrowers who recently transitioned from W-2 to self-employed in the same field. If you've been on your own less than two years and the work is similar to what you did before, ask specifically about 12-month programs.

The hardest case. If you started a completely new business with no prior history in that field and you're under two years, you're going to have a harder time. Not impossible, but harder. You may need to wait or look at non-QM products with higher down payments and stricter reserve requirements.

How Lenders Actually Calculate Your Income

This is where most self-employed buyers get caught off guard. Lenders do not use your gross income. They don't use your top-line revenue. They use your net income after expenses, and that number is usually significantly lower than what you actually feel like you make.

Conventional and FHA loans

For conventional and FHA loans, lenders pull your tax returns and use the net income from Schedule C (for sole proprietors), Schedule E (for partnerships and S-corps), or your K-1s. They average that net income over two years. If your most recent year is lower than the prior year, they may use the lower number. If your most recent year is higher, they typically use the average.

They will add back certain non-cash deductions: depreciation, depletion, business use of home (sometimes), and one-time expenses. But they will not add back your legitimate write-offs for vehicle expenses, supplies, contractor payments, or anything else that's actually leaving your bank account.

Here's the catch every self-employed buyer needs to internalize: the more aggressively you write off business expenses on your taxes, the less income you have available to qualify for a mortgage. If you wrote off $80,000 in expenses to lower your tax bill, you just told the mortgage lender you make $80,000 less than you actually take home.

Bank statement loans

Bank statement loans flip this entirely. Instead of using your tax returns, the lender uses 12 or 24 months of bank deposits and calculates your qualifying income from cash flow. A bank statement loan is a Non-QM mortgage that uses 12 or 24 months of bank deposits to calculate qualifying income instead of W-2s, pay stubs, or tax returns.

For business bank statements, lenders typically apply an "expense factor" (often 50%) to your deposits to estimate what's actually profit versus revenue. A CPA letter documenting actual expenses can improve this number with no minimum floor at Defy. If your CPA can document that your true business expense ratio is lower than 50%, your qualifying income goes up.

For personal bank statements, the calculation is more straightforward: deposits over the statement period, minus transfers between your own accounts, minus one-time deposits like tax refunds or gifts, divided by the number of months.

1099-only loans

A growing product category. Instead of bank statements or tax returns, the lender uses your 1099 forms directly. Griffin Funding uses 100% of the income from your most recent year's 1099(s) to qualify. You must have been contracted for at least two years. Some lenders count 90% rather than 100% of the 1099 amount to account for expenses, but the income calculation is faster and simpler than bank statement underwriting.

This product works well for real estate agents, traveling nurses on contract, full-time independent contractors who get most of their income from one or two clients, and anyone whose 1099 amounts genuinely reflect what they take home.

A Quick Note on "Non-QM" Before We Get Into Loan Products

I'm about to walk through six loan products, and three of them are described as "non-QM." Here's what that means, because the term gets thrown around without explanation.

Non-QM stands for Non-Qualified Mortgage. After the 2008 housing crisis, the Dodd-Frank Act created a category of mortgages called Qualified Mortgages (QM) with strict underwriting rules: tax-return-based income verification, debt-to-income ratios capped at 43%, no risky loan features like interest-only payments or negative amortization. Loans that follow these rules get legal protections for the lender.

A non-QM loan is any mortgage that doesn't fit inside those strict QM rules. It is not subprime, not predatory, not unregulated. It's a fully legal mortgage that uses alternative income documentation, like bank statements or 1099 forms, instead of tax returns. The lender takes on a little more risk, so the borrower pays a higher interest rate. Non-QM lending has been the fastest-growing segment of the self-employed mortgage market for the last several years, and most major lenders now offer these products either directly or through wholesale partners.

When you see "non-QM" below, think: legitimate mortgage, alternative documentation, slightly higher rate.

The Six Loan Products Available to Self-Employed Buyers in Atlanta

Here are the actual loan options, what they require, and who they fit.

1. Conventional loan (Fannie Mae / Freddie Mac)

The cheapest financing if you qualify. Standard 30-year fixed rates, down payments as low as 3% for first-time buyers and 5% otherwise.

Income documentation: Two years of personal tax returns, two years of business tax returns if applicable, year-to-date profit and loss statement, two months of bank statements.

Credit score minimum: 620, though 740+ unlocks the best rates.

Best for: Self-employed buyers whose tax returns reflect strong net income. If you don't aggressively write off business expenses, this is your best option.

The trade-off: Your net income drives your loan amount. If your tax write-offs are substantial, you may not qualify for as much house as you can actually afford.

2. FHA loan

Government-backed loan with more flexible credit and DTI requirements. 3.5% down payment with a credit score of 580 or above. 10% down with scores between 500 and 579.

Income documentation: Same as conventional. Two years of returns, P&L, bank statements.

Best for: First-time buyers with lower credit scores or higher debt-to-income ratios. FHA loans allow DTI up to 50% in many cases, where conventional usually caps around 45%.

The trade-off: Mortgage insurance is permanent for the life of the loan unless you put 10% or more down (in which case it falls off after 11 years). On a long horizon, that adds up.

3. VA loan

For eligible veterans, active duty, and qualifying surviving spouses. Zero down payment, no mortgage insurance, and competitive rates.

Income documentation: Two years of self-employment history with tax returns, P&L, bank statements.

Best for: Self-employed veterans. If you qualify for VA financing, this is almost always your best option regardless of how your tax returns look.

4. Bank statement loan (non-QM)

The most popular non-QM option for self-employed buyers in Atlanta right now. Qualify based on bank deposits instead of tax returns.

Income documentation: 12 or 24 months of personal or business bank statements, business license, sometimes a CPA letter or P&L.

Credit score minimum: Typically 640, though some programs start at 620. Most programs set minimums between 620-660. A borrower with 760 might receive a rate 1.5-2 percentage points lower than someone with 640.

Down payment: 10–25% depending on credit and loan size. Higher scores (720+) might qualify for 10-15% down. Scores 680-719 typically require 15-20%. Scores 660-679 often require 20-25%. Scores 620-659 may require 25%+.

Reserves: 3–12 months of mortgage payments held in liquid accounts after closing.

Interest rate: Higher than conventional. Bank statement loan rates are higher than conventional mortgage rates, typically 0.75–2.0% above prevailing 30-year fixed rates.

Best for: Self-employed buyers whose bank deposits significantly exceed their reported taxable income. If you write off a lot, this is often the difference between qualifying and not qualifying.

5. 1099-only loan (non-QM)

Similar to a bank statement loan but uses 1099 forms directly.

Income documentation: One to two years of 1099-NEC forms, year-to-date earnings statement or P&L, bank statements, ID, credit report.

Credit score minimum: 620–660.

Down payment: Typically 10–20%, with higher down payments for lower credit scores.

Best for: Independent contractors whose income is fully documented on 1099s. Real estate agents, traveling nurses on contract, sales professionals paid by 1099, contract consultants.

The trade-off: Higher interest rate than conventional. Make sure the income shown on your 1099s actually reflects your earning power before choosing this over a bank statement loan.

6. Profit & Loss (P&L) loan (non-QM)

The newest category in self-employed lending. Some lenders will qualify you based on a 12-month profit and loss statement prepared and signed by a licensed CPA or Enrolled Agent.

Income documentation: 12-month trailing P&L from a CPA or EA. Sometimes bank statements to validate.

Best for: Established business owners with clean financial statements but complex tax returns. Buyers who don't want to share 24 months of personal bank statements.

The trade-off: Generally the most expensive non-QM option. Limited lender availability. You need a CPA relationship.

What Your Tax Strategy Costs You in Buying Power

This is the conversation I have with self-employed buyers more than any other. Let me give you a concrete example.

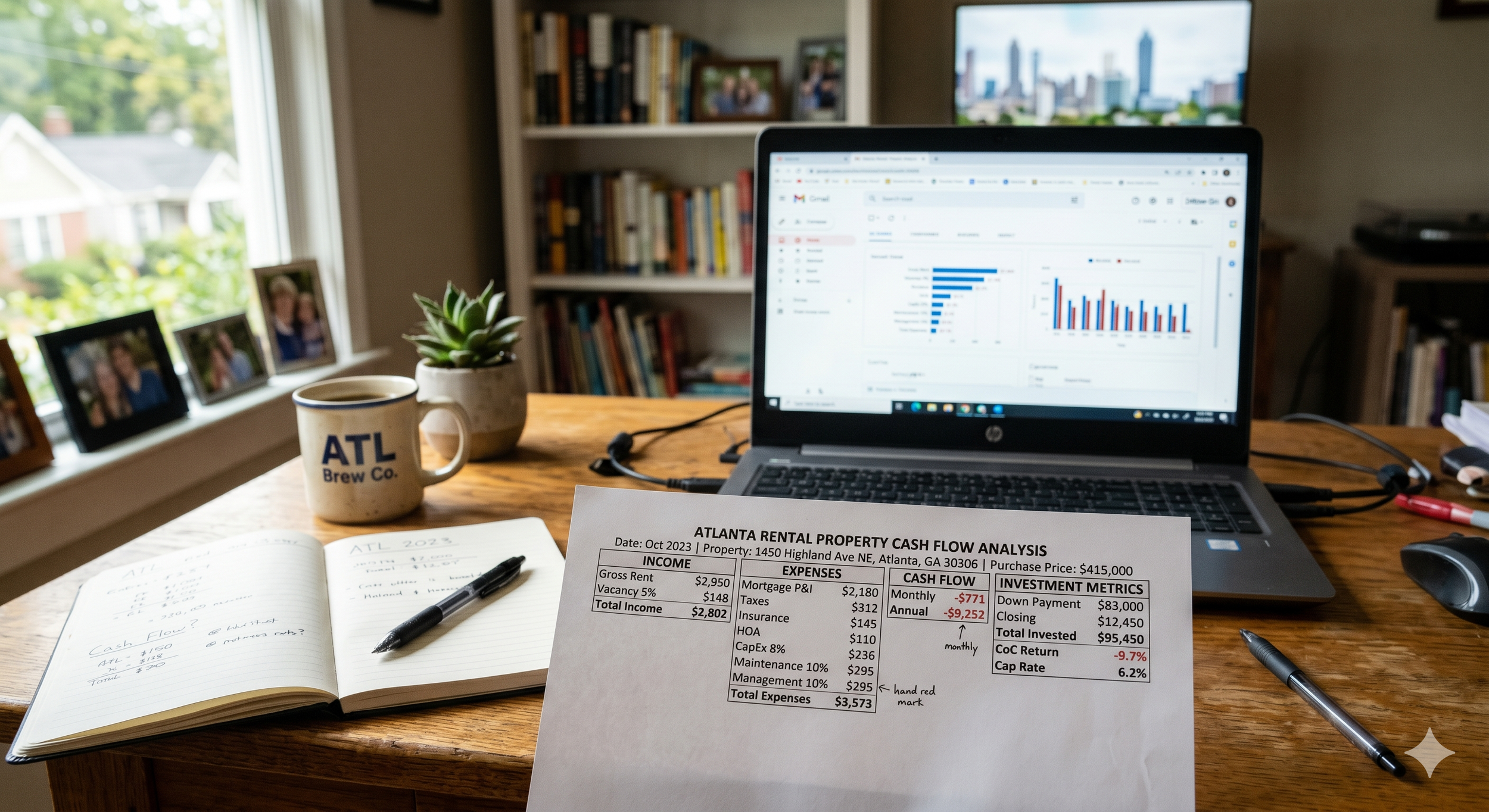

Imagine you're a freelance graphic designer in Atlanta. Your business brings in $180,000 a year. You write off $70,000 in legitimate expenses: home office, software, contractor payments to subs, travel, vehicle, equipment. Your Schedule C net income is $110,000.

A conventional lender will use that $110,000 figure (or the two-year average if it's different). At current rates and standard ratios, $110,000 in qualifying income gets you in the range of a $400,000–$450,000 home, depending on your other debt and down payment.

Now imagine the same designer with the same actual income, but writes off only $30,000 in expenses. Schedule C net is $150,000. Same buyer, same actual lifestyle, same cash flow. At $150,000 qualifying income, the buying range jumps to roughly $550,000–$620,000.

Same person. Same house they can actually afford. Different loan amount because of how the taxes were filed.

Here's the strategic question: if you know you want to buy a home in the next two years, the standard CPA advice to maximize write-offs may cost you more in lost buying power than it saves you in taxes. The math doesn't always favor aggressive write-offs when a home purchase is on the horizon.

Talk to a lender BEFORE your CPA finalizes your returns for the year. I cannot stress this enough. Get a sense of what income figure you need to support your target home price, and then make tax decisions with that information. Once the return is filed, you're stuck with it for the year.

The alternative is the bank statement loan path, which lets you keep your aggressive tax strategy and still buy at your real income level. But you'll pay more in interest. There's no free lunch in this trade-off, but you can pick which side of it makes more sense for your situation.

Documentation Checklist for Self-Employed Buyers

Whether you're going conventional or non-QM, the documentation lift is heavier for self-employed buyers. Start gathering this now:

For conventional and FHA:

Two years of personal federal tax returns, all schedules

Two years of business tax returns if you have a separate entity (1120, 1120-S, 1065)

Year-to-date profit and loss statement (signed)

Two most recent months of personal and business bank statements

Business license or articles of incorporation

Two years of 1099s if applicable

Two months of asset statements (retirement, investments, anywhere your reserves and down payment are sitting)

For bank statement loans:

12 or 24 months of consecutive bank statements (personal or business, depending on program)

Business license, articles of incorporation, or business filing

Year-to-date P&L statement

CPA letter if available (can lower your expense factor)

ID and credit report authorization

Asset statements for down payment and reserves

For 1099-only loans:

One to two years of 1099-NEC forms

Year-to-date earnings statement or P&L

Two months of bank statements

Business license or proof of contracting relationship

Asset statements

Always have ready, regardless of loan type:

Photo ID

Social Security card or ITIN documentation

Two years of address history

Explanation letters for any large or unusual deposits, gaps in employment, or credit blemishes

Credit Score Strategy for Self-Employed Buyers

Credit matters more for non-QM loans than it does for conventional. A 640 score will get you in the door for most bank statement programs, but a 720+ score will significantly improve your rate and reduce your down payment requirement.

Six to twelve months before you plan to buy:

Pull all three credit reports (Experian, TransUnion, Equifax) at annualcreditreport.com

Dispute any errors immediately

Pay down revolving credit card balances to below 30% of your limit, ideally below 10%

Do not close old accounts (length of credit history matters)

Do not open new credit accounts (each hard inquiry can drop your score)

Do not co-sign for anyone

Self-employed buyers often have higher utilization on business credit cards because they use them for business expenses. If those cards report to your personal credit, pay them down before applying. The lender's snapshot of your credit on the day they pull it is the snapshot they'll use, regardless of whether you typically carry that balance for a week before paying it off.

Down Payment and Cash Reserves: The Self-Employed Differentiator

Conventional loans for self-employed buyers don't require more down payment than they do for W-2 buyers. The 3%, 5%, 10%, 20% tiers all apply equally.

Non-QM loans are different. Bank statement and 1099 loans typically require 10–25% down, with higher down payments tied to lower credit scores or smaller loan files. The lender wants more skin in the game when they're relying on bank statements instead of tax returns.

Reserves are where self-employed buyers really feel the difference. Conventional loans for primary residences typically require zero to two months of reserves. Non-QM loans usually require 3–12 months of PITI (principal, interest, taxes, insurance) sitting in liquid accounts after you close.

That means if your mortgage payment is going to be $3,500 a month, a bank statement loan may require you to have $21,000–$42,000 sitting in savings or investments after you've paid your down payment and closing costs. That's on top of your down payment, not part of it.

This is the planning piece self-employed buyers most often underestimate. Don't drain your reserves to put more down. Keep liquid cash in place, even if it means a smaller down payment or a less expensive home.

Down Payment Assistance Programs in Georgia for Self-Employed Buyers

Georgia has solid down payment assistance options, and most of them are open to self-employed buyers as long as your loan qualifies.

Georgia Dream Homeownership Program. Up to $10,000 in down payment assistance, with additional amounts available for certain professions and locations. Income limits apply (typically around $97,000–$135,000 depending on household size and county). Must be a first-time buyer or have not owned a home in the past three years. Available for FHA, VA, USDA, and conventional loans.

Invest Atlanta down payment assistance. For homes purchased within the City of Atlanta limits, Invest Atlanta has several programs offering down payment and closing cost assistance, typically structured as forgivable second mortgages.

DeKalb, Cobb, Fulton, and Gwinnett county programs. Each county has its own program, with varying income limits and forgivable loan structures.

Most down payment assistance programs require a conventional, FHA, or VA loan as the first mortgage. They are not compatible with most non-QM bank statement or 1099 loans. If down payment assistance is critical to your purchase, you'll likely need to qualify on the conventional or FHA side.

When to Buy as a Self-Employed Buyer

The general advice that you can't perfectly time the market applies to self-employed buyers, but with one important addition: time your TAX returns, not the market.

The single best thing you can do is plan your purchase around your tax strategy. If you know you want to buy in the spring, talk to a lender in October or November of the prior year. They'll tell you what your debt-to-income looks like based on prior-year returns and current-year P&L, and you can decide with your CPA whether to leave more income on the table this year to support the purchase.

If you're going non-QM, the timing is less constrained by tax filing dates and more by your bank statement history. You'll want 12–24 months of clean deposits before applying, so don't drain accounts, move money around in ways you can't explain, or make large cash deposits without paper trails.

Common Mistakes Self-Employed Buyers Make

A few patterns I see repeatedly:

Not talking to a lender early enough. By the time you're house hunting, your tax returns are filed and your buying power is locked in. The conversation needs to happen six to twelve months before you want to close.

Picking the wrong loan product. Self-employed buyers often get pushed toward non-QM loans by mortgage brokers who specialize in them, even when conventional financing would be cheaper and available. Always price both options before choosing.

Mixing business and personal accounts. If your business deposits flow through your personal checking, your bank statement loan underwriting gets complicated fast. Separate accounts make the process cleaner and your qualifying income clearer.

Large unexplained deposits. Lenders will ask about any deposit over $1,000 that isn't a clearly identified payroll or invoice payment. Cash deposits, gifts, transfers from unfamiliar accounts. All of it requires documentation. Avoid making any deposits you can't explain in the 90 days before applying.

Quitting W-2 work right before buying. If you've been thinking about going independent, do not quit your W-2 job two months before you apply for a mortgage. Either buy first, then leave, or wait until you have at least one full year of self-employment income on a tax return.

Assuming the answer is no. I have buyers come to me convinced they can't qualify because someone told them three years ago that self-employed people can't get a mortgage. The non-QM market in 2026 is dramatically more accessible than it was even five years ago. Get an actual analysis before you assume you're out of the running.

Frequently Asked Questions

Can I buy a home in Atlanta if I just started a 1099 contract this year?

Generally, no, not with conventional financing. Most lenders want two years of self-employment history, or one year combined with two prior years of W-2 work in the same field. If you're under one year, your options narrow significantly. A few non-QM lenders will look at 12-month self-employment files for borrowers who transitioned from W-2 to self-employed in the same line of work, but expect higher down payments and stricter terms.

What credit score do I need to buy a home as a self-employed buyer?

For conventional loans, 620 is the floor and 740+ gets you the best rates. For FHA, 580 with 3.5% down or 500–579 with 10% down. For bank statement and 1099 loans, 620–640 is typically the floor, with 720+ unlocking the most favorable terms. Your credit score affects your rate, your down payment requirement, and how much house you can afford. Work on it well before you apply.

How many years of tax returns do I need to buy a home?

Two years is the standard for conventional, FHA, and VA loans. One year is sometimes acceptable if you transitioned from W-2 to self-employed in the same field and have two prior years of W-2 history. Bank statement loans typically need 12 or 24 months of bank statements, not tax returns. 1099-only loans typically need one to two years of 1099 forms.

Will my business write-offs hurt my mortgage application?

For conventional, FHA, and VA loans, yes. Significantly. Lenders use your net income after expenses, so every dollar of legitimate write-off is a dollar less in qualifying income. For bank statement loans and 1099-only loans, write-offs don't matter the same way because the lender isn't looking at your tax returns. This is the single biggest reason self-employed buyers choose non-QM financing.

What is a bank statement loan?

A bank statement loan is a non-QM mortgage that qualifies you based on 12 or 24 months of bank deposits rather than tax returns. The lender averages your deposits, applies an expense factor (typically around 50% for business accounts), and uses that figure as your qualifying income. It's designed for self-employed borrowers whose taxable income on paper is much lower than their actual cash flow.

How much down payment do I need as a self-employed buyer?

For conventional loans, the same as any other buyer: 3% for first-time conventional, 5% for standard conventional, 3.5% for FHA, 0% for VA. For non-QM loans like bank statement and 1099, expect 10–25% down depending on your credit score. Higher credit unlocks lower down payment requirements.

Are bank statement loans worth the higher interest rate?

It depends on the math. If a bank statement loan is the difference between buying now and waiting two more years, the higher rate is often worth it, especially if home prices and rates continue to move against you. If you could qualify conventionally with some planning around your tax strategy, conventional is almost always cheaper over the life of the loan. Always price both options before deciding.

Can I use a 1099 mortgage if I'm a real estate agent?

Yes. Real estate agents are some of the most common users of 1099 mortgage products. Your 1099s from your brokerage are typically the cleanest documentation of your income, and many lenders specialize in working with agents.

Can self-employed buyers use Georgia Dream or other down payment assistance?

Yes, as long as your underlying mortgage is a conventional, FHA, VA, or USDA loan and you meet the program's income limits and first-time buyer requirements. Non-QM loans like bank statement and 1099 loans are not compatible with most down payment assistance programs.

How long does it take to close on a home as a self-employed buyer?

Plan for 30–45 days from contract to close for conventional and FHA. Non-QM loans can sometimes close faster because they bypass the deeper tax return underwriting, but more commonly they take 35–50 days because the bank statement analysis adds time. Build the longer timeline into your offer if you're using non-QM financing.

Do I need a CPA to buy a home as a self-employed buyer?

You don't strictly need one, but it helps in two ways. A CPA can prepare a clean year-to-date profit and loss statement that lenders accept. For bank statement loans, a CPA letter documenting your actual business expenses can lower the expense factor the lender applies, which raises your qualifying income. If you're serious about buying and serious about your business, a CPA relationship pays for itself.

Should I incorporate my business before buying a home?

It doesn't help and can sometimes hurt. Incorporating creates a separate tax entity, which means lenders will want two years of business tax returns in addition to your personal returns. If you're under two years of incorporation, your business income may not count at all for conventional financing. If you're planning to buy in the next year or two, don't change your business structure right before applying.

Can I buy in Atlanta with mixed income (some W-2 and some 1099)?

Yes, and this is actually a strong file. If you have a W-2 job plus 1099 side income, lenders can use both sources. The W-2 income is easier to document and stable; the 1099 income adds to your qualifying figure. Just make sure the 1099 work has the two-year history requirement and that the W-2 job is solid and ongoing.

Working with Me as a Self-Employed Buyer

I've helped self-employed buyers across Metro Atlanta navigate every loan product on this list. I know which lenders close cleanly on bank statement files, which loan officers specialize in 1099 underwriting, and which programs match which buyer profiles. More importantly, I know how to structure your timeline so the loan side of your purchase doesn't fall apart at the worst moment.

If you're self-employed and starting to think about buying in Atlanta, whether you're a year out or a month out, let's talk early. The earlier we connect, the more options you'll have when it's time to apply.

Visit kristenjohnsonrealestate.com or reach out directly. Come as you are, come on home.

Looking for more Atlanta buyer education? I've covered How Much House Can I Afford in Atlanta, What Credit Score Do I Need to Buy a House in Atlanta, FHA vs Conventional Loan: Which Is Better in Atlanta, What Do I Need to Buy a House in Atlanta, and First-Time Home Buyer Mistakes to Avoid in Atlanta. Browse the full guide series at kristenjohnsonrealestate.com.