Assumable Mortgages in Atlanta: How Georgia Buyers Can Lock In a Seller’s Lower Rate in 2026

An assumable mortgage lets you take over the seller's existing FHA, VA, or USDA loan — including the original interest rate — instead of taking out a new mortgage at today's rates. With current Atlanta rates sitting in the mid-6% range, assuming a seller's 2.75% or 3% loan can cut your monthly payment by $800 or more on a $250,000 balance. The catch: only government-backed loans are assumable, you still have to qualify with the seller's lender, and you'll need to cover the difference between the purchase price and the remaining loan balance in cash or through secondary financing.

I work with buyers across Metro Atlanta, and assumable mortgages have moved from a niche topic to a real conversation piece over the last year. Right now there are over 280 assumable homes listed in Atlanta on platforms like Roam — FHA and VA loans carrying rates that were locked in during 2020–2022. If you're buying in the $300K–$550K range and the home was purchased with government financing a few years ago, it's worth asking.

Here's what you actually need to know.

Which Loans Are Assumable — and Which Aren't

FHA, VA, and USDA loans are assumable by law. Most conventional loans (Fannie Mae or Freddie Mac backed) are not — they include a due-on-sale clause that requires the loan to be paid off when the property transfers. That means if a seller bought with a conventional 30-year fixed in 2021 at 3.1%, that rate doesn't transfer to you.

The loans that do transfer are the government-backed ones:

FHA loans originated after December 15, 1989, are assumable. The buyer must meet standard FHA underwriting requirements — minimum 580 credit score, debt-to-income ratio that the lender accepts (FHA allows up to 50% in some cases), and documented income and employment. The lender charges an assumption processing fee capped at $1,800 since August 2024.

VA loans are also assumable, and here's something that surprises most buyers: you don't have to be a veteran to assume a VA loan. Any buyer who qualifies under the lender's credit and income standards can assume it. The buyer pays a 0.5% VA funding fee on the remaining loan balance (certain veterans and surviving spouses are exempt).

USDA loans are assumable as well, subject to lender approval and USDA income and property eligibility requirements.

One important thing for sellers with VA loans: if the buyer who assumes your loan is not a veteran, your VA entitlement stays tied to that loan until it's paid off. That affects your ability to use your full VA benefit on a future purchase. If you're a veteran planning to sell and then buy again using VA financing, talk to a VA-approved lender before you advertise your loan as assumable.

The Numbers: What the Savings Actually Look Like

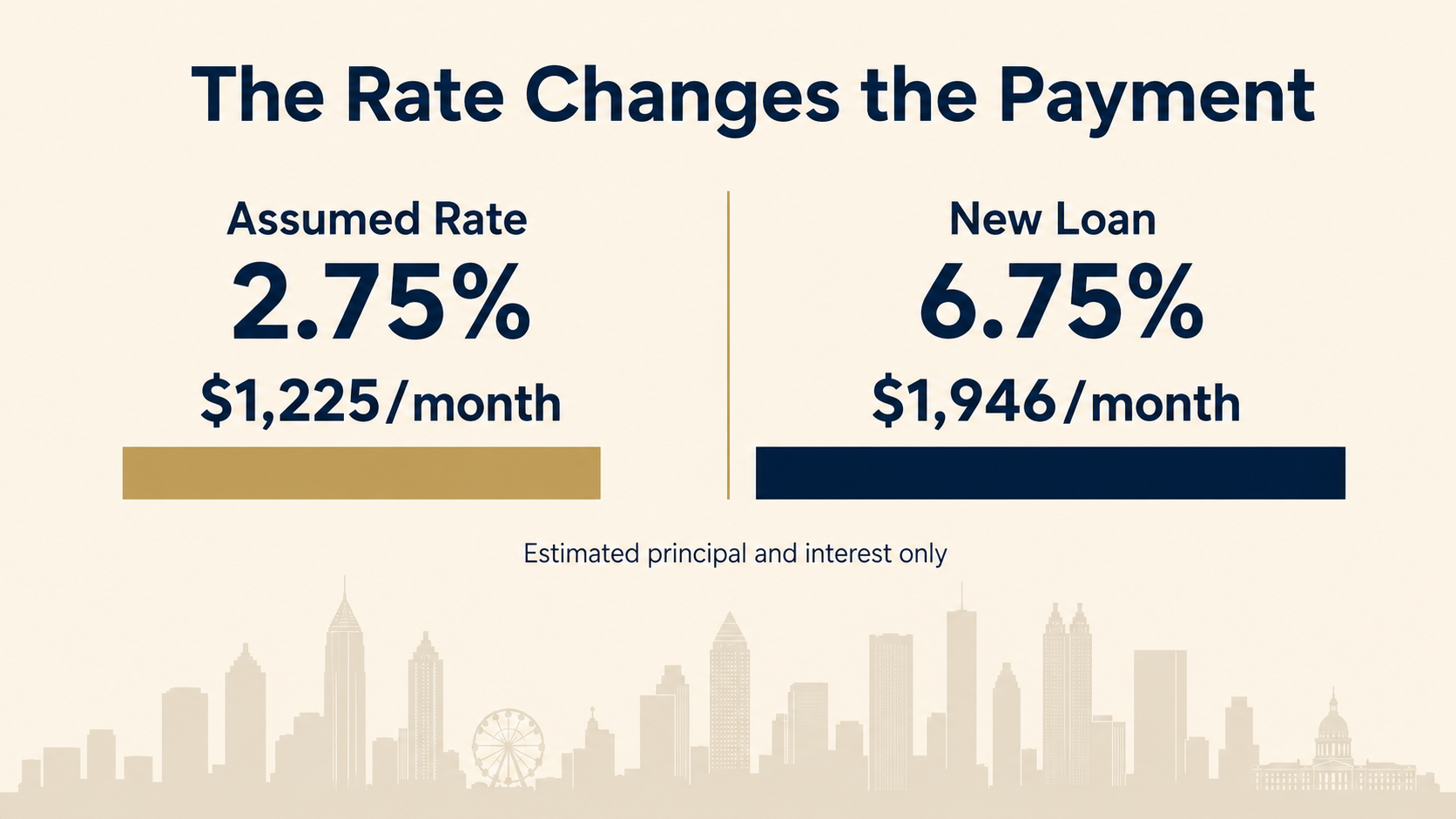

Let's make this concrete. Say a seller bought an Atlanta home in 2021 with a VA loan at 2.75% and the remaining balance is $250,000. You're buying the home for $400,000.

At 2.75% on $250,000, the principal and interest payment is around $1,020 per month.

If you take out a new loan for $320,000 (20% down on the $400,000 price) at today's rate of 6.75%, your payment is roughly $2,075 per month.

The math doesn't map perfectly because you're borrowing different amounts, but the rate difference alone on a $250,000 balance saves over $700 per month and more than $250,000 over the life of the loan. On a larger balance, the savings grow. Sources tracking this have quoted as much as $895 per month and $322,000 in total interest savings comparing a 3% assumed rate to a 6.5% new loan on the same balance.

That's real money. It's why assumption-specific platforms like Roam exist now, and why it's worth at least asking about the loan type every time you're looking at a home that could have been purchased with government financing.

The Equity Gap: The Part Most Buyers Don't Expect

The piece that trips people up is the equity gap. When you assume a mortgage, you take over the remaining balance. You don't borrow the full purchase price — you pay the seller the difference between the purchase price and what they still owe on the loan.

In the example above: $400,000 sale price minus $250,000 remaining loan balance = $150,000 you need to cover at closing. That $150,000 has to come from somewhere.

Three options:

Cash. The most straightforward but requires you to have that liquidity. Some buyers use proceeds from selling their current home toward the gap.

Gift funds. If family is contributing, standard gift letter documentation requirements apply and the servicer will verify the source.

Secondary financing (second mortgage). Some FHA and USDA assumptions allow a second lien to cover part of the equity gap. VA assumptions are trickier — VA guidelines don't permit a second mortgage in all cases. You'll need to confirm with the servicer before you make any assumptions about how you'll structure the gap.

The loan balance cannot be increased. There's no wrapping the equity gap into the assumption — you either come to closing with the funds or you have financing lined up to cover it.

This is where buyers sometimes run the numbers and find that assumption doesn't work for them on a specific property, even though the rate savings are significant. If the seller has substantial equity, the gap can be large enough that your cash requirements exceed a conventional down payment scenario. Run the math early with your lender.

How to Find Assumable Homes in Atlanta — and What the Process Looks Like

Finding them: A few approaches work.

Roam (withroam.com) is the most streamlined — it's a marketplace specifically for assumable FHA and VA listings and currently shows hundreds of Atlanta properties. AssumeList is another search tool. You can also check MLS data directly: the loan type is often listed, and any FHA or VA purchase from the last several years is worth a conversation.

The most underused tactic is simply asking. When you're making an offer on any home that could have been purchased with government financing — look at when it was bought, what the price range was, the neighborhood — have your agent ask the listing agent whether the seller's loan is assumable and what the remaining balance and rate are. Most sellers don't think to advertise it. Many agents on both sides don't raise it. That creates opportunity for buyers who are paying attention.

The process: Once you've identified a home with an assumable loan and you're under contract, here's what happens:

You apply directly with the seller's loan servicer — not a new lender of your choosing. You submit income verification, credit authorization, employment documentation, and bank statements. The servicer underwrites you under the relevant loan program's standards (FHA, VA, or USDA). If approved, the assumption closes through Georgia's standard attorney-managed process — same dry closing you'd have with any Georgia purchase, coordinated by the closing attorney.

Timeline: plan for 45 to 75 days. VA assumptions can stretch past 90 to 120 days. The servicer controls the pace, not you or your agent, which is the main variable to manage. If you have a firm move date, build in buffer. And do not sell your current home or give notice at a rental until you have a confirmed closing date.

Understanding the full Georgia closing process from contract to keys before you get under contract helps — assumption or otherwise, knowing what to expect makes the whole timeline easier to manage.

What Sellers With Low-Rate Loans Should Know

If you bought your Atlanta home in 2020–2022 with an FHA or VA loan, your assumable rate is a genuine selling advantage in 2026. In a market where buyers are price-sensitive and actively shopping rates, marketing your home's assumable 3% loan can draw attention and potentially support a stronger offer price.

A few things to sort out before you go that route:

Confirm with your loan servicer that the loan is eligible for assumption and what the current balance is. Your listing agent should be able to help you present this information clearly in the marketing materials.

If you have a VA loan and you want your entitlement restored after the sale so you can use VA financing again, the buyer ideally would also be a veteran with entitlement of their own to substitute. Otherwise, your entitlement stays encumbered. It's not a dealbreaker — plenty of sellers complete VA assumptions without entitlement substitution — but it's something to plan for with a VA-savvy lender before you list.

The seller disclosure process in Georgia doesn't require you to disclose loan terms, but being transparent about the loan details upfront streamlines the assumption process and prevents delays later.

Frequently Asked Questions

Do I have to be a veteran to assume a VA loan in Atlanta?

No. Any buyer who qualifies under the lender's credit and income standards can assume a VA loan in Georgia. You do not need to be a veteran or active-duty service member. The buyer pays a 0.5% funding fee on the loan balance at closing (some veterans and surviving spouses qualify for an exemption). The key is that you must qualify with the servicer — it's not a rubber stamp.

Can I assume a conventional mortgage from a seller?

Almost certainly not. Most conventional loans include a due-on-sale clause that requires full payoff when the property is sold. FHA, VA, and USDA loans are assumable. If you're shopping specifically for an assumable mortgage, focus on homes where the seller used government-backed financing, typically purchased between 2019 and 2022.

What credit score do I need to assume an FHA loan?

The standard FHA minimum is 580 with a 3.5% down payment (applied here toward the equity gap), though some lenders set their own overlays higher — 620 or 640 is common among servicers. You'll also need to meet the debt-to-income and income documentation requirements the servicer sets.

How do I cover the equity gap if I don't have that much cash?

The equity gap is the difference between the purchase price and the remaining loan balance. Options include cash from savings or home sale proceeds, gift funds from family (with proper documentation), or secondary financing where the loan program allows. VA assumptions are more restrictive about second mortgages. Confirm your financing plan with the servicer early — before you go under contract — so you're not caught off guard at closing.

How long does a mortgage assumption take to close in Georgia?

Plan for 45 to 75 days from contract to close for most FHA and USDA assumptions. VA assumptions can run 90 to 120 days or longer because the servicer controls the pace. Build buffer into your timeline and don't give notice at a rental or schedule a moving company until you have a confirmed closing date from the attorney.

Can the seller refuse to let me assume their mortgage?

If the loan is FHA or VA, the assumption right is built into the loan terms — but the servicer must approve you as the assuming buyer. The seller's cooperation is required to submit the assumption application, and they need to be motivated to go through the process. Most sellers who have a clearly assumable, low-rate loan and understand the marketing value are willing. If a seller declines to participate in the assumption process, you'd need to purchase with conventional financing instead.

Does the original mortgage term reset when I assume it?

No. You take over the loan where it is. If the seller is 4 years into a 30-year mortgage, you're inheriting a 26-year loan. That means your payoff date is earlier than a new 30-year mortgage, which is actually an advantage — you'll be building equity faster and paying interest for fewer years.

What are the closing costs on a mortgage assumption in Georgia?

You'll pay the servicer's assumption processing fee (capped at $1,800 for FHA loans since August 2024; 0.5% funding fee for VA on the assumed balance), plus standard Georgia closing costs — attorney fees, title search, recording fees. You'll also fund an escrow/impound account for property taxes and insurance if the servicer requires it. Your closing attorney will walk you through the full closing disclosure. You can get a general sense of what to expect from the Georgia buyer closing costs guide — most of those line items apply to assumption closings too.

If you're buying in Atlanta and want to know whether assumption makes sense for your situation — or if you're a seller with a low-rate government loan and want to think through how to position it — I'm happy to run through the specifics with you.

Schedule a consultation at kristenjohnsonrealestate.com/schedule and we'll talk through what the numbers actually look like for your move.

Kristen Johnson is a real estate agent and team lead with Kristen Johnson Real Estate at Compass Metro Atlanta. A native Atlantan who grew up in East Point and lives in Edgewood, she has guided clients through more than $50M in sales across the city and suburbs, drawing on a background as a labor doula that shapes her calm, clear, client-first approach. Connect with Kristen at kristenjohnsonrealestate.com.