Should I Buy a Home Now at 6%, or Wait for Rates to Drop? An Atlanta Buyer's Guide for 2026

If you are sitting on the sidelines waiting for mortgage rates to fall before you buy, here is the honest answer: waiting is a bet, not a plan, and it is a bet that has lost money for most Atlanta buyers over the last three years.

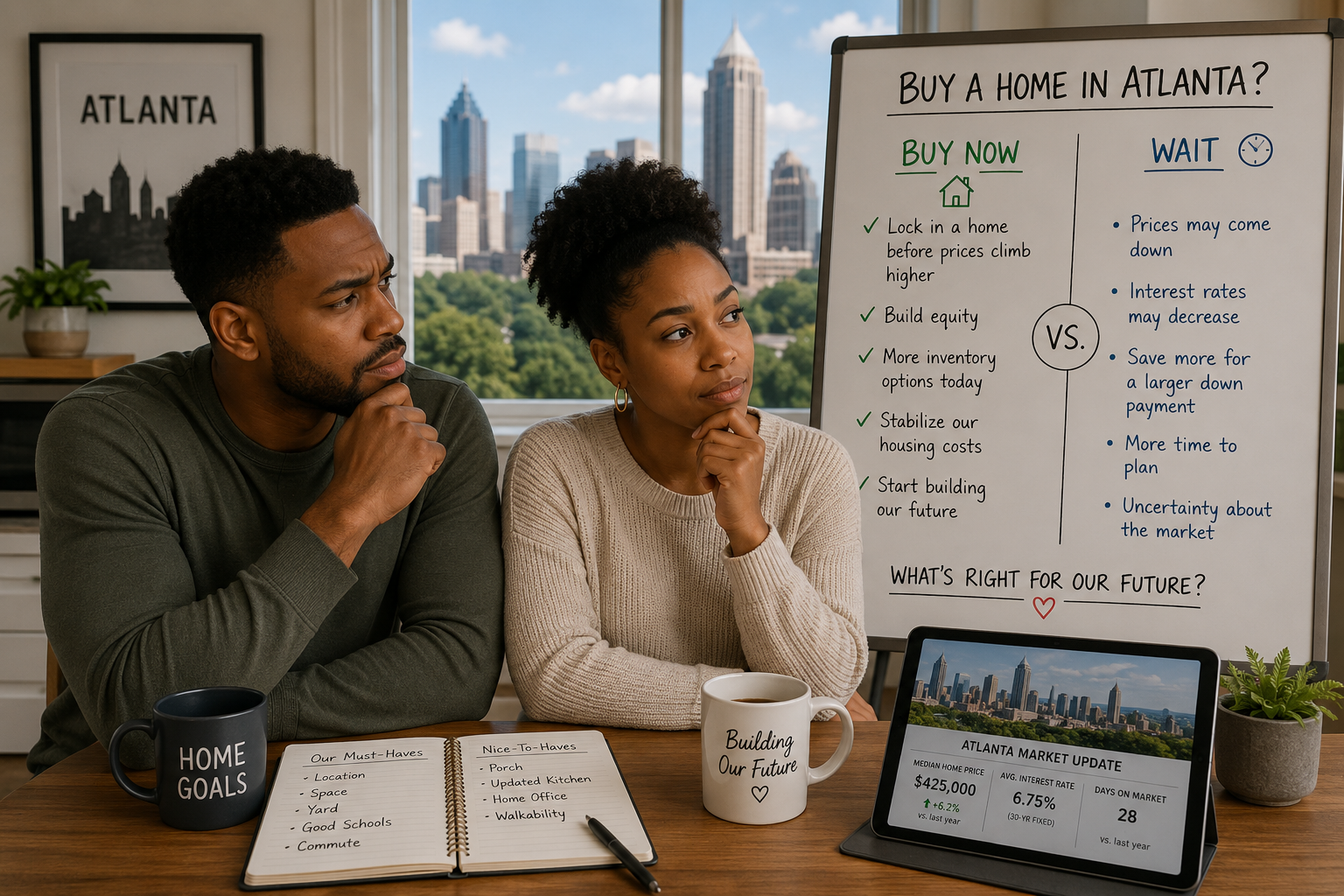

I work with buyers across Metro Atlanta, and this is the single most common question I get right now. Rates have been hovering in the 6 percent range, and almost everyone wants to know the same thing. Should I lock in now, or hold out for something better? It is a fair question. A mortgage is the largest financial commitment most people ever make, and a percentage point feels like it should matter enormously.

Nearly a decade of helping Atlanta buyers has taught me that the rate question is rarely the right question. The right question is whether buying makes sense for your life and your budget at the rate available today, because that is the only rate you can actually act on.

Here is what you need to know.

The Quick Answer: What "Waiting for Rates" Actually Costs

Let me give you the direct version before we get into the details.

Nobody can reliably predict mortgage rates. Not the Federal Reserve, not Wall Street, not me, and not the lender who tells you rates are "definitely coming down." The people whose entire job is forecasting rates have been wrong repeatedly over the last three years. In late 2024, the Fed cut its benchmark rate three times, and mortgage rates went up afterward, not down. If the professionals cannot time it, you cannot either.

When rates drop, home prices tend to rise. Lower rates pull more buyers off the sidelines at the same time. Those buyers compete for the same houses, and competition pushes prices up. So the buyer who waited for a better rate often ends up paying more for the house, with a larger loan, and faces bidding wars that did not exist when rates were higher. The discount you waited for gets eaten by the price increase you did not see coming.

You can change your rate later. You cannot change your purchase price. This is the part most buyers miss. If you buy at 6 percent and rates fall to 5 percent in two years, you refinance and capture the lower rate. If you wait and prices rise 8 percent while you sit out, you are locked into that higher price for the life of the loan. Rates are temporary. Purchase price is permanent.

So when buyers ask me whether to buy now or wait, my answer is not "buy now" as a blanket rule. My answer is this: decide based on whether you can comfortably afford the home at today's rate and today's price. If you can, waiting mostly exposes you to risk. If you cannot, no rate forecast fixes that, and the work is on the budget side, not the timing side.

That is the short version. Now let me show you the reasoning, the numbers, and how this plays out specifically in the Atlanta market.

Where Mortgage Rates Actually Stand in 2026

First, some context, because a lot of buyers are anchored to numbers that are no longer accurate.

During the height of the pandemic, mortgage rates fell to historic lows, with some buyers locking 30-year fixed loans under 3 percent. Those rates were a crisis-era anomaly. They were the product of emergency monetary policy, and they are not the baseline that normal markets return to. If your mental picture of a "good" mortgage rate is 3 percent, you are comparing today's market to a once-in-a-generation event that is unlikely to repeat.

In 2023, rates climbed sharply, touching nearly 8 percent at their peak. That was the other extreme. Through 2025 and into 2026, rates settled into a more stable band, generally in the 6 percent range for a 30-year fixed loan. The exact number moves week to week, and your personal rate depends heavily on your credit score, down payment, loan type, and the lender you choose, so I am not going to quote a single figure that will be stale by the time you read this. Talk to a lender for a real quote tied to your actual profile.

Here is the more useful point. Rates have been relatively flat for over a year. They have not been spiking, and they have not been crashing. They have been sitting in a range. That stability is actually good news for buyers, even though it does not feel like it. It means you can plan. You can shop, get pre-approved, look at homes, and lock a rate without the ground shifting under you every week.

The forecasts for the rest of 2026 mostly point to rates staying in roughly the same range, with some economists expecting modest movement lower and others expecting them to hold. A few firms have floated the high 5 percent range as a possibility. None of them are forecasting a return to anything close to pandemic lows. So if you are waiting for a dramatic drop, you are waiting for something that the people who study this for a living are not predicting.

A note on data: rate figures and forecasts change constantly, and any number in a blog post is a snapshot, not a guarantee. For a current rate quote and a current forecast, talk to a lender, and reach out to me for where the Atlanta market stands the week you are reading this.

Why Lower Rates Do Not Mean a Better Deal

This is the piece of the puzzle that most "wait for rates" advice ignores, and it is the most important piece.

The housing market is a system. Mortgage rates are one input, but they are not the only input. Home prices respond to supply and demand, and demand responds to rates. When rates fall, buying gets cheaper on a monthly basis, so more buyers can qualify and more buyers feel comfortable jumping in. All of those buyers arrive in the market at roughly the same time, chasing roughly the same homes.

The result is predictable. More competition. More multiple-offer situations. More homes selling above asking. Less negotiating room. The buyer-friendly conditions that exist in a higher-rate environment, where sellers are more willing to negotiate and offer concessions, tend to evaporate when rates drop and demand surges.

So picture two versions of the same buyer.

Buyer A purchases a home in Atlanta today at a 6 percent rate. The market has more inventory than it did a few years ago, sellers are more open to negotiation, and Buyer A has room to ask for a price reduction, a closing cost credit, or a repair concession after inspection.

Buyer B waits 18 months for rates to fall. Rates do drop, but so do the buyer-friendly conditions. Buyer B is now competing with a wave of other buyers who also waited. The home Buyer B wanted has appreciated. Buyer B writes three offers before winning one, pays at or above asking, and gets no concessions. The lower rate is real, but the larger loan balance and the lost negotiating leverage cancel a meaningful part of it.

This is not a hypothetical I made up. It is the pattern that has played out repeatedly. Buyers who waited for a better rate frequently ended up worse off, because they got the lower rate and a higher price at the same time. The rate was the thing they were watching. The price was the thing that actually moved the math.

Run the Numbers: A Percentage Point Is Smaller Than You Think

Buyers consistently overestimate what a rate difference does to a monthly payment. Let me show you with real math, using a round number so it is easy to follow.

Say you are buying a home and financing a loan amount of $360,000, which is a realistic figure for a good portion of the Metro Atlanta market after a typical down payment. Here is the monthly principal and interest payment at three different rates on a 30-year fixed loan.

| Interest Rate (30-Yr Fixed) | Monthly Principal & Interest | Difference vs. 6.0% |

|---|---|---|

| 5.5% | $2,044 / month | $111 less per month |

| 6.0% | $2,158 / month | Baseline |

| 6.5% | $2,275 / month | $117 more per month |

Based on a $360,000 loan amount, 30-year fixed, principal and interest only. Does not include taxes, insurance, or HOA. Figures are illustrative; get a personalized quote from a lender.

The jump from 6 percent to 6.5 percent is about $117 a month. The drop from 6.5 percent down to 5.5 percent, a full point, is about $228 a month. A full percentage point on a $360,000 loan is roughly $230 in monthly payment. That is real money, and I am not going to pretend it is not. Over 30 years it adds up.

But here is the context that matters. If you are waiting for a full point of improvement, you are waiting for something the forecasts do not currently predict. And while you wait, if Atlanta home prices rise even 4 to 5 percent, which is in line with what several forecasts project for the year, the home you wanted costs roughly $15,000 to $20,000 more. That price increase means a bigger loan, a bigger down payment to hit the same percentage, and a higher payment that partly or fully erases the rate savings you were chasing.

And remember the asymmetry. If you buy at 6 percent today and rates fall to 5.5 percent in two years, you refinance. You capture the lower payment without having paid the higher price. The buyer who waited cannot undo the higher purchase price. Ever.

This is why I tell buyers to focus on whether the payment works at today's rate. If a home is comfortably affordable for you at 6 percent, you are in a strong position. If it is a stretch at 6 percent, the honest conversation is about your budget and your price range, not about a rate forecast.

What the Atlanta Market Looks Like Right Now

Rates are a national story. Real estate is local. Here is where Metro Atlanta actually stands, because the buy-or-wait decision depends on local conditions, not just the national rate headline.

Inventory has been climbing for three consecutive years. Active listings across Metro Atlanta are meaningfully higher than they were during the supply crunch of 2022 and 2023. More homes on the market means more choices for you and less of the desperate, sight-unseen, waive-everything bidding that defined the pandemic market. Months of supply has been moving up year over year, which is the technical way of saying the market has shifted toward a more balanced position.

Prices have been relatively stable. The median sale price across Metro Atlanta has held in a range, with modest movement rather than dramatic swings, depending on the month and the data source you look at. This is not a market that is crashing, and it is not a market that is booming. It is a market that is functioning at a more normal, sustainable pace.

Homes are taking longer to sell. Average days on market across the metro has stretched well beyond the frenzy years, often north of 60 days. For a buyer, longer days on market is leverage. It means you have time to think, time to do a proper inspection, and room to negotiate on a home that has been sitting.

Atlanta has repeatedly been named one of the more buyer-friendly major markets in the country, specifically because of this combination of improving inventory and moderating price growth.

Now, the important nuance, because "Metro Atlanta" is not one market. It is dozens of micro-markets that behave differently.

| Market Type | Conditions in 2026 | Buyer Leverage |

|---|---|---|

| Well-priced homes in top intown neighborhoods and competitive school zones | Still see strong demand; well-presented homes can sell quickly, sometimes with multiple offers | Limited; move decisively and be pre-approved |

| Mid-market homes across the metro | More inventory and longer days on market than recent years; more balanced conditions | Moderate; room to negotiate price and terms on the right home |

| Outer suburbs and homes that have been sitting on the market | Elevated inventory, extended days on market, more price reductions | Strong; real room for price cuts, credits, and repair concessions |

Conditions vary by neighborhood and price point. Contact Kristen for a read on your specific target market.

The takeaway is that buyer leverage in Atlanta right now is real but uneven. In well-priced homes in the most in-demand intown neighborhoods and top school zones, you may still see competition and quick sales. In outer suburbs and on homes that have been sitting, you have genuine negotiating room. A blanket "the whole market favors buyers" statement is too simple. The right answer depends on the specific price point and the specific area, which is exactly the kind of read I give buyers I work with.

When Waiting Actually Does Make Sense

I am not going to tell you that buying immediately is always right. That would be the same lazy advice as "always wait," just pointed in the other direction. There are real situations where waiting is the correct, responsible choice. Here they are honestly.

Wait if you are not financially ready. If buying at today's rate and today's price would leave you with no emergency fund, no cushion for repairs, or a payment that consumes too much of your income, then you should wait. But understand what you are waiting for. You are not waiting for rates. You are waiting until your finances are in a position where homeownership is sustainable. That is a budget timeline, not a market timeline, and it is entirely within your control. Use the time to pay down debt, build savings, and strengthen your credit score, which will also get you a better rate when you do buy.

Wait if your life is genuinely unsettled. If your job situation is uncertain, if you might relocate within a year or two, or if you are not sure where in Metro Atlanta you want to plant roots, buying is risky regardless of the rate. The transaction costs of buying and then selling within a short window can wipe out any benefit. Homeownership rewards staying put. If you cannot commit to a few years in one place, renting is the responsible choice.

Wait if you have not done the homework. If you have not been pre-approved, have not talked to a lender about your actual numbers, and have not figured out what you can realistically afford, you are not ready to buy. That is fixable in a few weeks, and it should be the first thing you do.

What is not on this list: waiting purely because you think rates will be lower next year. That is the one reason to wait that I will push back on every time, because it treats an unpredictable forecast as if it were a plan, and it ignores what happens to prices and competition when rates do fall.

If you are financially ready, settled in your life, and have done the homework, then the rate environment is not a reason to sit out. It is just the cost of borrowing money right now, and it is a cost you can revisit through a refinance later.

How to Buy Smart at 6 Percent

If you have decided to move forward, here is how to make a 6 percent rate work harder for you. There are real tools, and most buyers do not use them.

Negotiate a rate buydown. In a market with more inventory and motivated sellers, you can often negotiate for the seller to pay points that buy your interest rate down. A temporary buydown lowers your rate for the first year or two. A permanent buydown lowers it for the life of the loan. Builders especially are often willing to do this on new construction. This is one of the strongest tools available right now, and it is a negotiation, so it requires an agent who knows how to ask for it.

Shop your lender. Rates and fees vary between lenders, sometimes significantly, for the exact same borrower. Get quotes from at least three. The difference between a good quote and a lazy one can be a quarter point or more, which is real money. I can connect you with lenders I trust who will give you straight numbers.

Strengthen your own rate. Your rate is not just the market rate. It is the market rate adjusted for your credit score, your down payment, and your debt load. Improving your credit score before you apply, and putting more down if you can, will move your personal rate down without the market moving at all.

Negotiate the price and the terms. This is where current Atlanta conditions help you. On a home that has been on the market a while, you have room to negotiate the price down, ask for closing cost credits, or request repairs after inspection. Those concessions are worth real money and they are easier to win now than they will be if rates drop and competition surges.

Plan to refinance. Buy the house at a payment you can afford today. If rates fall meaningfully in the next few years, you refinance and capture the lower rate. Marry the house, date the rate, as the saying goes. The house is the long-term commitment. The rate is not.

Buy the right house, not the perfect-timing house. The home that fits your life, your commute, and your budget is worth far more to you than a hypothetical quarter-point you might catch if you guess the market correctly. Buyers who get fixated on timing often miss the actual house.

The Honest Bottom Line

Here is what I tell every buyer who asks me this question.

You cannot time the mortgage market. The professionals cannot do it, and chasing it usually costs you more than it saves, because prices and competition move against you exactly when rates improve.

What you can control is your own readiness. Your budget. Your credit. Your savings. Your clarity about where you want to live and for how long. Those are the things that determine whether buying is a good decision, and not one of them is a rate forecast.

If you are financially ready and you find the right home at a price that works at today's rate, waiting mostly exposes you to risk: the risk of higher prices, more competition, and lost negotiating leverage. If you are not ready, no rate environment fixes that, and the work is on your finances, not on the calendar.

Six percent is not a crisis rate. It is, by historical standards, a fairly normal rate. The sub-3 percent era was the anomaly, not the rule. Buyers have purchased homes and built wealth at 6, 7, and 8 percent for decades. The question was never the rate. The question is whether the home and the payment fit your life.

Frequently Asked Questions

Should I buy a house now or wait for mortgage rates to drop in Atlanta?

If you are financially ready, settled in your life, and can comfortably afford the payment at today's rate, waiting mostly exposes you to risk rather than reward. When rates drop, more buyers enter the market and home prices and competition tend to rise, which often cancels out the savings from the lower rate. If you are not financially ready, then waiting makes sense, but you are waiting on your own budget and savings, not on the rate market. The decision should be based on your readiness, not a rate forecast.

Will mortgage rates go down in 2026?

Most forecasts for 2026 expect rates to stay roughly in the 6 percent range, with some economists predicting modest movement lower into the high 5 percent range and others expecting rates to hold. None are forecasting a return to anything close to pandemic-era lows. Rate forecasts have been wrong repeatedly over the last few years, so I would not build a home-buying plan around any specific prediction. For a current forecast and a real rate quote tied to your profile, talk to a lender.

Is 6 percent a high mortgage rate?

By the standards of the last few years it feels high, because buyers are anchored to the sub-3 percent rates of the pandemic. But those rates were a crisis-era anomaly. Looking at the longer history of the U.S. mortgage market, rates in the 6 percent range are fairly normal. Buyers have purchased homes and built equity at 6, 7, and 8 percent for decades.

If I buy now at 6 percent, can I refinance later if rates drop?

Yes. If rates fall meaningfully after you buy, you can refinance into a lower rate. This is the key reason the rate matters less than buyers think. You can change your rate later through a refinance, but you cannot change your purchase price. If you wait and prices rise, you are locked into the higher price for the life of the loan. Refinancing does have closing costs, so it makes the most sense when the rate drop is large enough to justify them, but the option exists.

Why do home prices go up when mortgage rates go down?

Lower rates make monthly payments cheaper, so more buyers can qualify and more buyers feel ready to act. All of those buyers enter the market at roughly the same time and compete for the same homes. That surge in demand pushes prices up and brings back multiple-offer situations. It is the reason waiting for a lower rate often backfires: you get the rate, but you also get higher prices and more competition.

What is the Atlanta housing market like for buyers in 2026?

Metro Atlanta has seen inventory rise for three consecutive years, which gives buyers more choices and more negotiating room than during the 2022 and 2023 supply crunch. Prices have been relatively stable, and homes are taking longer to sell, often more than 60 days on average. Atlanta has been named one of the more buyer-friendly major markets in the country. That said, conditions vary widely by neighborhood and price point. Well-priced homes in top intown neighborhoods and competitive school zones can still move quickly, while outer suburbs and homes that have been sitting offer more leverage.

How much does a 1 percent difference in mortgage rate actually cost?

On a $360,000 loan, a full percentage point is roughly $230 per month in principal and interest. That is real money over 30 years. But it is often smaller than buyers expect, and it can be outweighed by a price increase while you wait. If Atlanta prices rise 4 to 5 percent during the time you sit out, the home costs roughly $15,000 to $20,000 more, which means a bigger loan and a higher payment that can erase the rate savings. The exact figures depend on your loan amount, so run your own numbers with a lender.

What is a mortgage rate buydown and can I get one in Atlanta?

A rate buydown is when points are paid upfront to lower your interest rate, either temporarily for the first year or two or permanently for the life of the loan. In the current Atlanta market, with more inventory and motivated sellers, you can often negotiate for the seller to pay for a buydown as a concession. Builders are frequently willing to do this on new construction. It is one of the most effective tools available to buyers right now, and it is a negotiation, so it helps to work with an agent who knows how to structure the ask.

Should first-time buyers wait for lower rates?

Not as a default. First-time buyers are often the most tempted to wait, but they are also the most exposed when prices rise, because they are usually buying at the more competitive lower price points. If you are financially ready, the better move is usually to focus on what you can control: improving your credit score, saving for your down payment, researching down payment assistance programs, and getting pre-approved. If you are not yet financially ready, then use the waiting time to get there. The waiting should be tied to your finances, not the rate market.

What should I do right now if I am thinking about buying?

Start with three steps. First, talk to a lender and get pre-approved so you know your real numbers and your actual rate, not a headline figure. Second, get honest about your budget, your savings cushion, and how long you plan to stay in the home. Third, talk to an agent who knows the specific Atlanta submarkets you are considering, because leverage and competition vary dramatically by neighborhood and price point. Those steps tell you far more about whether to buy than any rate forecast will.

Let's Talk

The buy-now-or-wait question is rarely about the rate. It is about your finances, your timeline, and the specific corner of the Metro Atlanta market you are looking at. I work with buyers across the metro, from first-time buyers to move-up buyers to investors, and I will give you an honest read on whether buying makes sense for you right now, and a clear plan if it does.

Visit kristenjohnsonrealestate.com or reach out directly. Come as you are, come on home.