What Is a 1031 Exchange and How Does It Work for Atlanta Investors in 2026?

A 1031 exchange lets you sell an investment property and roll the proceeds into another investment property without paying capital gains tax at the time of sale. The tax is deferred, not erased. You hand the equity from your sold property to a Qualified Intermediary, identify your replacement within 45 days, close on it within 180 days, and the IRS treats the whole transaction as a continuous investment rather than a taxable sale.

That is the short version. The long version matters more, especially in Atlanta, where the math, the timeline, and the inventory dynamics can make or break a deal that looked clean on paper.

I work with buyers and investors across Metro Atlanta. A meaningful share of my deals involve someone exchanging out of a rental, a small multifamily, or a long-held property they inherited or bought a decade ago when the numbers worked differently than they do now. The 1031 exchange is one of the most powerful tools in real estate, and it is also one of the easiest to fumble if you go in without a plan.

Nearly a decade of helping Atlanta investors means I have seen exchanges work beautifully and I have seen them fall apart in the 45-day window because someone underestimated how tight the inventory is in the price band they needed.

Here's what you need to know.

What a 1031 Exchange Actually Is

Section 1031 of the Internal Revenue Code allows you to defer federal capital gains tax when you exchange one piece of real property held for business or investment use for another. The Tax Cuts and Jobs Act of 2017 narrowed this to real estate only. Personal property, equipment, vehicles, and similar assets no longer qualify. Real estate held for investment or business use is what we are talking about for the rest of this post.

The mechanics work like this. You sell a property you have held for investment. Instead of taking the cash, the proceeds go directly to a Qualified Intermediary, also called a QI or accommodator. You identify replacement properties in writing within 45 calendar days of closing on your sale. You close on one or more of those identified properties within 180 calendar days of your original sale. If you follow every rule, the IRS treats the transaction as an exchange, not a sale, and you defer the capital gains tax you would have owed.

The word defer matters. You are not avoiding the tax permanently. You are pushing it down the road, often indefinitely. Many investors chain 1031 exchanges across multiple properties over decades. When they eventually pass the property to heirs, those heirs receive a stepped-up basis at the fair market value as of the date of death, and the accumulated deferred gain can be wiped out entirely. That is the real long-game strategy. The exchange itself is the tool. Generational wealth is the goal.

The Tax Math: What You Actually Save in Georgia

Most investors underestimate how much they save in a 1031 exchange because they forget about everything beyond the headline federal capital gains rate.

Here is what you defer when you complete a valid exchange on a Georgia investment property in 2026:

Federal long-term capital gains tax. For long-term holds of more than one year, the federal rate is 0 percent, 15 percent, or 20 percent depending on your taxable income bracket. Most real estate investors land in the 15 percent or 20 percent range.

The 3.8 percent Net Investment Income Tax. This applies to investors with modified adjusted gross income above $200,000 single or $250,000 married filing jointly. It stacks on top of the capital gains rate.

Georgia state income tax on the gain. Georgia does not have a separate capital gains tax. Instead, capital gains are taxed as ordinary income at the state's flat rate. For 2026, that rate is 5.39 percent, and it is scheduled to step down annually toward a target of around 4.99 percent by 2029 under HB 1437, subject to revenue triggers.

Depreciation recapture. If you have been depreciating the property on your tax returns, the IRS recaptures that depreciation at a 25 percent rate when you sell. This is often the biggest tax bill people forget about, and it is deferred in a 1031 exchange along with the capital gain.

Here is a real example. Say you own a Decatur rental you bought in 2015 for $250,000. You have depreciated $50,000 of it over the years. Today, it sells for $525,000. Your adjusted basis is $200,000 ($250,000 minus $50,000 in depreciation), so your gain is $325,000.

In a straight sale at a 15 percent federal rate, you would owe roughly $48,750 in federal capital gains tax plus $12,350 in depreciation recapture, plus $17,517 in Georgia state income tax on the full gain. That is north of $78,000 before you account for selling costs, transfer tax, and the 3.8 percent NIIT if it applies. A 1031 exchange defers all of it.

That deferred tax stays in your buying power. Instead of reinvesting $446,000 after taxes, you reinvest the full $525,000. Compounded over a few exchanges across a couple of decades, the difference is substantial.

Georgia-Specific Rules You Need to Know

Georgia conforms to IRC Section 1031 without modification. That means a properly structured federal exchange also defers your Georgia tax. You file the federal Form 8824 with your federal return and report the deferred gain on your Georgia Form 500. There is no separate state exchange form to file.

A few Georgia-specific details that matter:

Non-resident withholding. Under O.C.G.A. Section 48-7-128, when a non-resident sells Georgia real estate, the closing attorney is required to withhold 3 percent of the sales price and remit it to the Georgia Department of Revenue. If you are exchanging into Georgia from another state and then exchanging back out as a non-resident, you complete Georgia Form IT-AFF2, the Affidavit of Seller's Gain, to apply for an exemption or reduced withholding. File this with the buyer before closing. If you do not, that 3 percent comes off the top and you have to claim it back on a Georgia non-resident return.

Georgia transfer tax. Georgia imposes a real estate transfer tax of $1 per $1,000 of consideration paid by the buyer at closing. This is among the lowest transfer taxes in the country and does not meaningfully affect exchange economics, but it is a line item you will see on your closing statement.

No state estate tax. Georgia does not have a state estate or inheritance tax. Combined with the federal stepped-up basis at death, Georgia real estate held through chained 1031 exchanges is one of the more tax-efficient long-term wealth strategies available to investors.

State filing requirements. Some states, including California, Massachusetts, Montana, and Oregon, enforce clawback rules that require ongoing reporting when an investor exchanges out of that state. Georgia does not. If you exchange out of a Georgia property into a property in another state, you do not have to file annual Georgia returns to keep tracking the deferred gain. You file the federal Form 8824 in the year of the exchange and you are done at the state level until you eventually sell the replacement property in a taxable transaction.

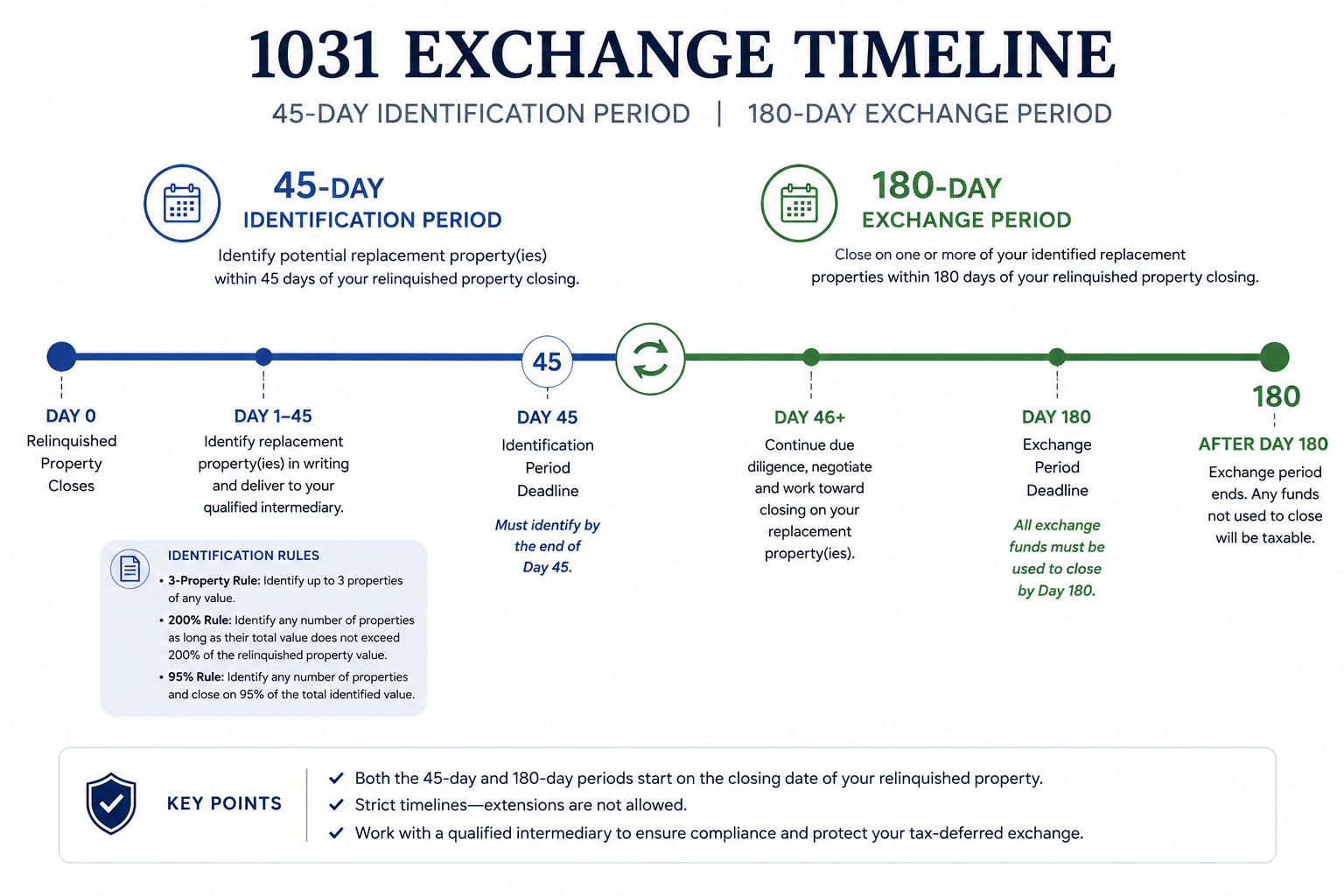

The 45-Day and 180-Day Rules

The two clocks run at the same time. They do not stack. The day you close on your sale is Day 0. The 45-day identification window and the 180-day completion window both start on Day 1.

Day 45. By midnight of Day 45, you must deliver a written, signed identification of your potential replacement property or properties to your QI. You cannot deliver it to your real estate agent or your attorney. It has to go to the QI or another qualified party. The IRS does not extend this deadline for weekends, holidays, or natural disasters except in very narrow federally declared emergency situations under Revenue Procedure 2018-58.

Day 180. By Day 180, you must close on one or more of your identified replacement properties. Same rule. No extensions.

There is one trap that catches Q4 sellers every year. The 180-day window is actually the earlier of 180 days or your federal tax filing deadline for the year of the sale. If you close on your relinquished property in October, November, or December, your 180 days will run past April 15 of the following year. If you do not file an extension on your tax return, your exchange period automatically ends on April 15, not on Day 180. That can cut your timeline by weeks or months. Anyone selling investment property in Q4 needs to file IRS Form 4868 to extend their tax return and preserve the full 180-day window.

Identification Rules: How Many Properties You Can Name

You cannot identify an unlimited list of replacement properties and pick one later. The IRS uses three rules under Treasury Regulation Section 1.1031(k)-1(c)(4), and you can use only one per exchange.

The 3-Property Rule. You identify up to three potential replacement properties of any value. This is what most individual investors use. You can name three properties, then close on one, two, or all three.

The 200% Rule. You identify any number of properties as long as the combined fair market value does not exceed 200 percent of the value of the property you sold. If your relinquished property sold for $500,000, your combined identified properties cannot exceed $1,000,000.

The 95% Rule. You identify any number of properties of any value, but you must close on properties totaling at least 95 percent of the combined identified value. This is rarely used because the bar is so high.

Most Atlanta investors I work with use the 3-Property Rule. Three is enough to give you backup options if your first choice falls through during due diligence.

What Qualifies as Like-Kind in Real Estate

"Like-kind" is broader than most people think. For real estate, almost any U.S. investment property can be exchanged for almost any other U.S. investment property. The properties do not have to match in type, use, or class.

You can exchange:

A single-family rental in East Atlanta for a fourplex in Decatur

A small office building in Midtown for raw land in North Georgia

A short-term rental near the BeltLine for a strip retail center in Gwinnett

A duplex in Kirkwood for a fractional interest in a Delaware Statutory Trust (DST)

What does not qualify:

Your primary residence (that is Section 121, not Section 1031)

A property you flip (held primarily for sale, not investment)

Property held outside the United States in exchange for U.S. property

Personal-use property, including second homes that do not meet investment-use criteria

Stocks, bonds, partnership interests, or other securities

The "held for investment or business use" requirement is what trips up the most people. If you bought a rental and never actually rented it, or you tried to use the property personally before exchanging, the IRS can disallow the exchange. Most tax advisors recommend holding the replacement property as a rental for at least two full tax years before considering any conversion to personal use.

The Qualified Intermediary: Why You Need One

You cannot touch the sale proceeds at any point during the exchange. If you do, even briefly, the entire exchange is disqualified and you owe the full tax bill. The Qualified Intermediary, sometimes called an accommodator or exchange facilitator, exists to hold the funds between your sale and your purchase.

The QI:

Prepares the exchange agreement and assignment documents

Receives the sale proceeds directly from the closing attorney

Holds the funds in a segregated account during the exchange period

Receives your written identification on Day 45

Wires funds to the closing attorney for your replacement property purchase

The IRS has specific rules about who cannot serve as your QI. Your real estate agent, your attorney, your accountant, or anyone who has acted as your agent in the past two years is a "disqualified person" under the regulations. The QI has to be a neutral third party. You cannot use someone who works for you.

Choosing a reputable QI matters more than most investors realize. Your money sits in their account for up to 180 days. There have been cases over the years where QIs went out of business or misappropriated funds and exchangers lost everything. Use an established, bonded QI with strong financial assurances. Ask for proof of fidelity bonds, errors and omissions coverage, and segregated account arrangements. This is not where you want to save $500 by choosing the cheapest option.

I have a short list of QIs I work with regularly in Atlanta. If you need a referral, reach out.

The Five Types of 1031 Exchanges

Most investors only ever do one type, but it helps to understand the options.

Delayed (Forward) Exchange. This is the standard. You sell first, then buy within 180 days. About 95 percent of exchanges are structured this way.

Simultaneous Exchange. Both properties close on the same day. Simple in concept, hard to coordinate in practice. Still requires a QI for compliance.

Reverse Exchange. You buy the replacement property first, then sell the relinquished property within 180 days. An Exchange Accommodation Titleholder takes title to the new property while you arrange the sale. This is more complex and significantly more expensive, with QI fees often running $5,000 to $15,000 above a standard exchange. Useful when you have found a once-in-a-cycle replacement property and cannot wait to sell first.

Improvement Exchange (Build-to-Suit). You use exchange funds to make improvements or build on the replacement property before taking title. The improvements have to be completed within the 180-day window. Specialized and complex.

Delaware Statutory Trust (DST). Not a separate type of exchange, but a structure that qualifies as like-kind replacement property. A DST is a fractional ownership interest in institutional-grade real estate, often a portfolio of apartment complexes, industrial properties, or net-lease retail. DSTs let investors who do not want to actively manage another property place their exchange equity into passive ownership of a larger asset. They have downsides: limited liquidity, no operational control, and management fees that erode returns. They are most useful as backup identification properties on Day 45 in case your primary replacement deal falls through.

Understanding Boot

"Boot" is the part of an exchange that does not qualify for tax deferral. If you receive anything other than like-kind property in the exchange, that something is boot, and it is taxable in the year of the sale.

Two common forms of boot:

Cash boot. If you sell a property for $500,000 and only spend $450,000 on the replacement, the extra $50,000 is cash boot. The IRS taxes it.

Mortgage boot (debt relief). If your sold property had a $300,000 mortgage and your replacement property has a $250,000 mortgage, the $50,000 reduction in debt is treated as boot. Most investors do not realize this until it is too late.

The rule of thumb to avoid boot: trade up or equal in both total purchase price and total debt. If you sell a $500,000 property with a $300,000 mortgage, you need to buy a replacement of $500,000 or more with a mortgage of $300,000 or more. If you trade down on either number, the difference becomes taxable.

Why a 1031 Exchange Makes Sense in Atlanta Right Now

The Atlanta investor landscape in 2026 looks different than it did even three years ago. Two structural shifts matter.

Inventory has loosened.The Atlanta Realtors Association reported a median sales price across Metro Atlanta of $411,000 in September 2025, with inventory increasing modestly compared to the historically tight supply of 2022 and 2023. That gives investors more breathing room than they had during the pandemic-era frenzy, but the 45-day clock still applies. Loosening inventory does not mean unlimited time.

Rent growth has cooled. Atlanta rent growth in 2026 is tracking 2 to 4 percent annually, well off the double-digit gains of the post-pandemic years. Insurance costs are up 20 to 40 percent across many submarkets, and property tax reassessments in hot zones like Fulton, DeKalb, and Cobb are pushing operating costs higher. The investors who do well in this environment are the ones who buy for cash flow at current rents, not projected future rents.

A 1031 exchange is particularly useful right now for three categories of Atlanta investors:

Investors who have ridden the appreciation wave. If you bought a rental in 2014, 2015, or 2016 for $200,000 to $300,000, it is probably worth $450,000 to $700,000 today depending on the submarket. The gain on paper is large, but the cash flow on a property that has appreciated that much is often weak because rents have not kept pace. Exchanging into a multi-unit property in South Fulton or Gwinnett, or into multiple smaller properties in higher cash-flow corridors, can reset the cash flow without triggering the tax bill.

Investors consolidating from multiple smaller properties. Three single-family rentals scattered across the metro can become one small apartment building or one duplex plus one renovated single-family in a stronger rental market. The exchange lets you simplify operations and concentrate equity without paying tax on the appreciation.

Out-of-state investors exchanging into Atlanta.Atlanta has consistently ranked among the top commercial real estate markets in the country, with lower price-per-unit multifamily values than coastal markets like California and New York. I work with investors from higher-tax states who are exchanging out of California or New York rentals and into Atlanta because the math on cash flow, taxes, and entry price all favor the move.

Where Atlanta Investors Are Exchanging Into in 2026

These are the submarkets I see drawing the most exchange interest right now. None of this is a recommendation. Every investor's situation is different and you should run your own numbers before committing.

South Fulton. Median home prices in the $200,000 to $280,000 range with rents of $1,500 to $1,800 produce the strongest gross yields in the metro. Proximity to Hartsfield-Jackson and the growing commercial corridor along Camp Creek support long-term demand.

Gwinnett County. Lawrenceville, Lilburn, Norcross, and Duluth all offer solid rent-to-price ratios. Buford has emerged as a strong choice for investors who want appreciation upside along with cash flow. The school districts in northern Gwinnett continue to draw families, which supports tenant retention.

Established intown rental markets.Grant Park, East Atlanta, Kirkwood, and Reynoldstown command higher rents but also higher acquisition prices. These work best for investors prioritizing tenant quality, long hold periods, and appreciation alongside cash flow.

Westside corridor.West End, Adair Park, and Oakland City sit along the BeltLine Westside Trail. Entry prices are lower than the eastside, appreciation has been strong, and the rental market continues to develop as the trail and adjacent commercial corridors mature.

Decatur.The City of Decatur and the surrounding DeKalb County submarkets attract long-term tenants who value walkability and access to MARTA. Cash flow is tighter at these price points, but tenant retention is strong.

How to Plan an Exchange Before You List

The biggest mistake I see is investors who list their rental, accept an offer, and then start thinking about a 1031 exchange. By that point, the clock has already started counting down in the back of their mind, and they are scrambling for replacement properties before they have a strategy.

The right sequence:

Start with the tax conversation. Talk to your CPA before you do anything else. Confirm your basis, your depreciation schedule, and what your tax bill would actually be in a straight sale. Sometimes the answer is that the tax hit is small enough that a 1031 is not worth the complexity. More often, the answer is that the deferral is meaningful and worth pursuing.

Identify your replacement strategy before you list. Know what you are exchanging into in broad terms before you start the sale. Are you consolidating? Diversifying? Moving from single-family into multifamily? Geographic shift? Cash flow focus or appreciation focus? Decide this before you have 45 days on a clock.

Engage your QI early. Reach out to your Qualified Intermediary before your relinquished property goes under contract. The QI prepares the exchange documents that need to be in place at closing. This is not something you set up at the last minute.

Pre-shop replacement properties. Once you have a buyer for your relinquished property and a closing date in sight, start actively looking for replacement properties. Make offers, even contingent ones. The goal is to have a clear path to identification by Day 45, not to be searching from scratch.

File your tax extension if needed. If you are closing in Q4, file Form 4868 with the IRS in March or early April of the following year to preserve your full 180 days. Talk to your CPA about timing.

When a 1031 Exchange Does Not Make Sense

It is not the right tool for every investor or every transaction. A few situations where I have advised against it:

The tax bill is small. If you have not held the property long enough to accumulate significant depreciation or appreciation, the deferral may not justify the complexity and fees of the exchange.

You actually want the cash. A 1031 exchange forces you to reinvest in real estate. If you need liquidity for another purpose, retirement, business investment, college tuition, paying off debt, the exchange takes that option off the table.

You are exiting real estate. If your long-term plan is to leave real estate investing entirely, the deferral just postpones the inevitable. Sometimes paying the tax now is the right answer, especially if you expect to be in a higher tax bracket later.

You cannot identify a quality replacement in 45 days. Forcing yourself into a marginal property to meet the deadline is a worse outcome than paying the tax on a clean sale. I have seen investors take bad deals to save a tax bill, and the bad deal hurts more in the long run.

The replacement property cash flows worse than the relinquished property. The exchange should improve your portfolio, not just preserve tax basis. If you cannot identify a replacement that is operationally better, you are deferring tax to acquire a worse asset.

Common Mistakes That Kill Exchanges

A few patterns I have seen invalidate otherwise straightforward exchanges:

Touching the money. Even briefly. Even if the closing attorney accidentally wires the funds to you instead of the QI. The IRS calls this constructive receipt and it disqualifies the exchange. This is why the cooperation language in the sale contract matters and why the QI documents have to be signed before closing.

Missing the 45-day deadline. Calendar mistakes, vacation timing, replacement deals that fell through and left no time to find others. The deadline does not extend for any reason short of a federally declared disaster.

Identifying too many properties without using the right rule. Naming five properties without staying under the 200 percent rule disqualifies the entire identification.

Buying from a disqualified person. Using a related party as the seller of the replacement property can disqualify the exchange. The IRS has specific holding requirements for related-party transactions.

Title mismatch. The taxpayer who sold the relinquished property must be the same taxpayer who buys the replacement property. If you sell as an individual and try to buy in your LLC, the exchange fails unless the LLC is a disregarded entity for tax purposes.

Trading down on price or debt. Boot is taxable. If your replacement property is smaller or has less debt, you will pay tax on the difference.

Frequently Asked Questions

What is a 1031 exchange in simple terms?

A 1031 exchange lets you sell an investment property and reinvest the proceeds into another investment property without paying capital gains tax at the time of the sale. The tax is deferred, not eliminated. You have 45 days to identify a replacement property and 180 days to close on it.

Can I do a 1031 exchange on my primary residence in Atlanta?

No. A 1031 exchange only applies to property held for investment or business use. Primary residences fall under Section 121, which is a different tax provision that excludes up to $250,000 of gain for single filers or $500,000 for married couples filing jointly, as long as you have lived in the home for at least two of the past five years.

How much does a 1031 exchange cost in Georgia?

Standard delayed exchanges typically run $750 to $1,500 in QI fees, plus normal closing costs on both transactions. Reverse exchanges and improvement exchanges cost significantly more, often $5,000 to $15,000 above a standard exchange. There are no separate Georgia state filing fees because Georgia conforms to the federal rules.

Does Georgia conform to the federal 1031 exchange rules?

Yes. Georgia fully conforms to IRC Section 1031. A properly structured federal exchange defers both your federal capital gains tax and your Georgia state income tax on the gain. You file the federal Form 8824 and report the deferred gain on your Georgia Form 500. There is no separate state exchange form.

What is the Georgia state capital gains tax rate in 2026?

Georgia does not have a separate capital gains tax. Capital gains are taxed as ordinary income at the state's flat rate, which is 5.39 percent in 2026. Under HB 1437, the rate is scheduled to step down annually toward approximately 4.99 percent by 2029, subject to revenue triggers.

Can I exchange a rental property in Atlanta for a property in another state?

Yes. The like-kind requirement refers to the nature of the property, real estate for real estate, not its geographic location. You can exchange an Atlanta rental for a property in Florida, Texas, or any other state. As long as both properties are held for investment or business use in the United States, the exchange qualifies.

What happens if I miss the 45-day identification deadline?

The exchange fails and the original sale becomes a fully taxable transaction. You owe capital gains tax and depreciation recapture on the entire gain in the year of the sale. The IRS does not grant extensions for the 45-day deadline except in very narrow federally declared disaster situations.

Can I use 1031 exchange funds to make improvements to a property I already own?

Not directly. You can structure an Improvement Exchange (also called a Build-to-Suit Exchange) where exchange funds are used to make improvements on a replacement property before you take title, but the improvements have to be completed within the 180-day window and the property has to be one you acquire through the exchange, not one you already own.

How many times can I do a 1031 exchange?

There is no limit. Many investors chain exchanges across multiple properties over their lifetime, deferring tax each time. Each exchange transfers the basis of the relinquished property to the replacement, so the deferred gain compounds. The most tax-efficient endpoint is holding the property until death, when heirs receive a stepped-up basis at fair market value and the accumulated deferred gain is eliminated.

Can I do a 1031 exchange into a vacation home or short-term rental?

Yes, if the property is genuinely held for investment use. The IRS has issued safe-harbor guidance (Revenue Procedure 2008-16) that allows short-term rental properties to qualify if you rent them at fair market rental for at least 14 days per year and limit personal use to 14 days per year or 10 percent of rental days, whichever is greater, for at least two years.

What is a Qualified Intermediary and why do I need one?

A Qualified Intermediary is a neutral third party who facilitates the exchange by holding the sale proceeds from your relinquished property and using them to acquire your replacement property. The IRS requires a QI because you cannot have constructive receipt of the funds at any point during the exchange. Your real estate agent, attorney, accountant, or anyone who has acted as your agent in the past two years cannot serve as your QI.

Can I 1031 exchange into a Delaware Statutory Trust (DST)?

Yes. DST interests qualify as like-kind replacement property. A DST is a fractional ownership interest in institutional-grade real estate, often used by investors who want to defer tax without taking on active management of another property. DSTs have downsides including limited liquidity and no operational control, so they are not right for every investor.

How does depreciation recapture work in a 1031 exchange?

When you sell a depreciated property in a straight sale, the IRS recaptures the depreciation you have claimed and taxes it at a 25 percent rate. In a 1031 exchange, depreciation recapture is deferred along with the capital gain. The depreciation schedule carries over to the replacement property, which means your future depreciation deductions on the replacement property are lower than they would be on a freshly acquired property of the same value.

I work with investors across Metro Atlanta on both ends of 1031 exchanges, helping clients sell relinquished properties and source replacement properties within the 45-day window. If you are thinking about exchanging out of a property in 2026 or relocating investment capital into Atlanta from another market, let's talk before you list.

Visit kristenjohnsonrealestate.com or reach out directly. Come as you are, come on home.

Looking for more Atlanta investor and buyer education? Read Is Now a Good Time to Buy a House in Atlanta, How Much House Can I Afford in Atlanta, and Negotiating in the 2026 Atlanta Market. Browse the full guide series at kristenjohnsonrealestate.com.